A solar PV system is a big purchase, and most of us will make use of a solar loan to complete the purchase for various reasons. Maybe you just want to get the system with zero out-of-pocket. Maybe you just need to finance a portion of the cost. And very often we just want the monthly payments to be at the level of an average electric bill so the funds can be diverted from purchasing electricity to paying for the solar system. Read on to get familiar with the options and the cost associated with solar loans.

Most solar installers will offer financing through some partners, unless the solar installer is large enough to vertically integrate a financing division, i.e. Sunrun or Tesla.

Here is the main point: When you finance a solar system you are really buying two products or services. That is true even when using in-house financing. One product is the solar PV system and the other is the financing. Both of these have costs and profits to the provider.

The solar purchase

Let’s talk about one of those two products, the solar system. The cost of it is in the labor and parts associated with producing electricity form the sun and making this available for your home. That is design, permits, interconnect, materials, installation and commissioning. All of these are included in the cash quote for your system. That’s it. In other words, that is the cost of your system. You should always ask for a cash quote even if you are planning to finance the system. That is how you can separate the cost of the solar product from the financing product.

The financing

The lender issuing a solar loan to you will normally have two ways to cover their cost and take a profit for the risk associated with lending money. Those are: a) Originating fees and b) Loan interest. The latter is calculated using an Annual Percentage rate (APR).

Originating fees

If you have a mortgage or you have refinanced a home loan then you are familiar with origination fees. Which are normally bundled in the closing costs. This is the cost that the lending organization will incur in order to issue you a loan. For example, doing all the required paperwork and validating your credit worthiness. In some cases, the originating fee also include some profit for the lender.

Solar loans also have origination fees although they may be called by other names; dealer fees, convenience fee, finance fee, Etc. but, essentially, perform the same function. Some solar dealers will add this fee to the cost of the solar system and then calculate the monthly payments as one product. You, as a savvy consumer, need to be aware of this additional cost. For that reason, you should ask for a cash quote for the same system and compare it to the financed quote.

Some partner lenders require that this originating fee not be disclose the consumer, as it is a “dealer’s fee” instead of a “consumer’s fee” but in reality, the solar dealer is working in a competitive market and cannot absorb this cost, and thus, pass it along to the consumer.

The dishonest dealer

The honesty issue here is not with the fee but how it is hidden or embedded into the cost of the solar system. The fee is a consequence of the loan, and the loan provide benefits for the consumer. Thus, the consumer needs to be aware of it and its size so they can take action. There are plenty of options for the consumer. For example: Higher interest loans with smaller fees, home equity loans, mortgage refinance, personal loans and Local credit union loans.

Here is how to spot a dishonest solar dealer:

- He or She won’t give you a cash estimate for the solar system if they know you will finance it.

- The dealer gives you a cash estimate and a finance estimate but, the financed estimate increases the cost of the solar system with no mention of finance fee (dealer fee).

- Both the cash and finance estimate are the same but the finance interest (APR) is below market rate. …more on this below.

Annual Percentage Rate (APR)

The APR is a percentage of the yearly balance that the lender will charge you for the unpaid balance. Money cost money. In other words, the lender typically will borrow the funds from the federal bank at certain APR to then lend it to you at a higher APR while keeping a small portion (the difference) as a profit.

Let’s assume that a bank called “Good Bank and Savings” borrowed $100k from the federal bank at a 5.00% APR. In order for Good Bank to make a profit it needs to lend this $100k at a higher APR than 5.00%. Lending it for the same or below 5.00% would represent a loss of money and without another form of profit Good Bank would go bankrupt.

Because of this simple math, when you see a finance offer with an APR bellow market rate, you can tell that somewhere else there is an additional cost and profit hidden in the product you are financing. For this reason, if you see a cash estimate with the same system cost as a financed estimate with an a ridiculously low APR, you will know that the cash estimate was inflated to cover the finance fee (dealer fee) of the finance option, so they both look equal.

What is expected, if the cash estimate is equal to the financed estimate, is an APR that is a few fractions of points higher than the market rate. If the federal interest rate is at 7% then you can expect an APR of 7.75% in your solar finance estimate and no dealer or finance fees. That is in case you have a fantastic credit score. If you credit score is less than perfect then you can expect a point or two higher than the federal APR rate.

The whole picture

Solar loans, originating fees and interest rates are all useful in one way or another. You just need to understand their function and how to use them so you don’t fall in a trap of the fast talker solar dealer.

The most economical way to purchase a solar PV system is still with cash. Financing can be used in several options and conditions, according to your needs. Let’s examine two hypothetical consumers cases: both Mark and John want to buy the same $20,000 solar PV system and both have an average electric monthly bill of $200. The current federal interest rates is at 6.25% APR.

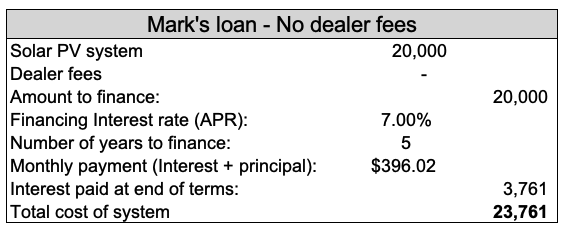

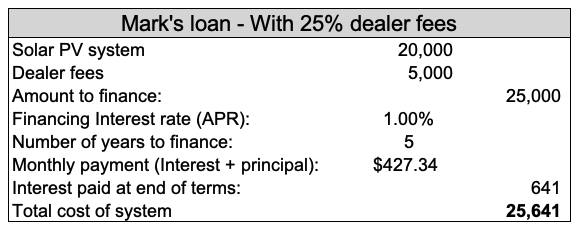

Case 1 - Mark's loan options:

Mark has good credit and employment history. The credit agency gave him a 700+ credit score. Mark can add up to $300 to his current monthly expenses.

To reduce the total cost of the system and only add about $250 to Mark’s total monthly expenses Mark is financing the system for 5 years. Here are his options with dealer’s fees and without.

Mark’s options analysis:

The no-dealer fee option is better for Mark despite having a higher interest rate of 7% which is aligned to the market. This option results in a lower monthly loan payment and a lower total system cost of $23,761. Instead of $25,641 of the option with dealer fees.

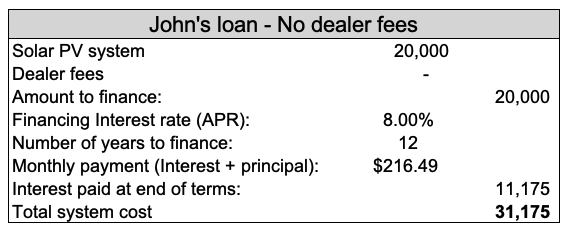

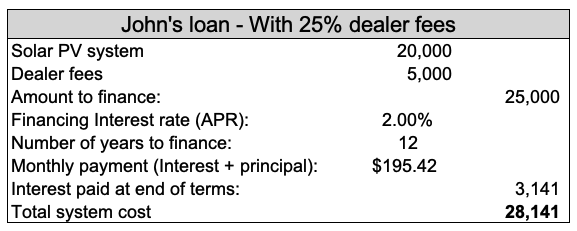

Case 2 - John's loan options

John has good credit and employment history. The credit agency gave him a 600+ credit score and John wants to keep his current monthly expenses the same.

To keep John’s monthly expenses the same, his solar loan payment must stay around $200 monthly, which is close to his electric bill savings from the solar system. Because of this John financed his system for 12 years. Here are his options with dealer’s fee and without.

John’s options analysis: The option with dealer fee is better for John. He paid $5,000 to lower his APR to 2% which is below market level. Because of that, this option results in a lower monthly loan payment and a lower total system cost of $28,141. Instead of $31,175 of the option with no dealer fees.

To complicate matters more, we need to say that financing with dealer’s fee, as demonstrated here, has the least savings if the loan is paid early, i.e. before the 12 years. In the case of John with the dealer’s fee built into the loan, making advance payment the most he can save is a portion of the $3,141 on interest which is significantly less than the no-dealers fee option which has $11,175 in interest over the life of the loan.

We work with lending partners which use originating fees and some which do not. It all depends of your preference. What you will get from our finance options is full disclosure. You will have all the information in order to make the right decision for you.

As always, we are energy experts no financial experts. The information presented here is not to be used as financial advice. Please check with your accountant for advance and recommendations on solar financing.